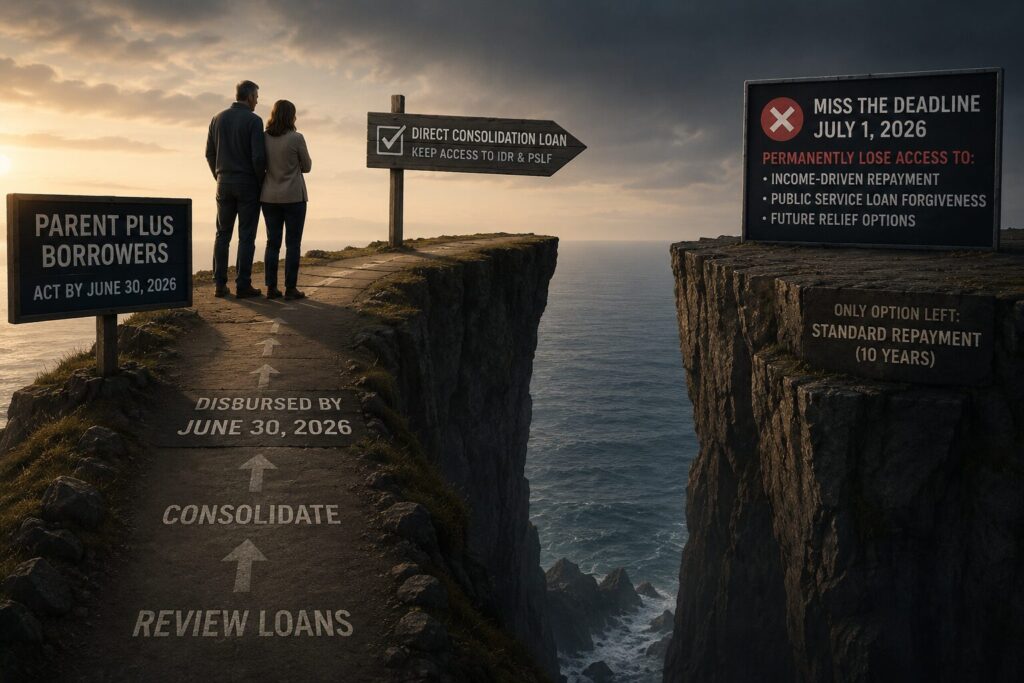

The Parent PLUS Cliff: Who Has Until June 30, and What Happens If They Miss It

Parent PLUS borrowers who do not have a Direct Consolidation Loan disbursed before July 1, 2026 lose permanent access to income-based repayment. Not “until they fix it.” Permanently. Income-Contingent Repayment (ICR) sunsets June 30, 2028. The Repayment Assistance Plan (RAP) that replaces most federal repayment options on July 1, 2026 explicitly excludes Parent PLUS and any consolidation loan that includes Parent PLUS funds. This is a one-shot deadline, and most of your clients who borrowed for their children don’t know it’s coming.

The planning window to catch this is measured in weeks. The advisor who runs a scan of their book for Parent PLUS borrowers this month becomes the only person in those clients’ financial lives who flagged it.

What “the cliff” actually is

The One Big Beautiful Bill Act (P.L. 119-21) changed the rules for Parent PLUS borrowing in two ways. Starting July 1, 2026, new Parent PLUS loans are capped at $20,000 per year and $65,000 lifetime per dependent student, a sharp departure from the prior cost-of-attendance-based ceiling. That’s the borrowing side, which matters for current college parents.

The repayment side is the cliff. For existing Parent PLUS borrowers, the transition rules are narrower than they appear in most summaries. Parent PLUS loans have never been directly eligible for income-driven repayment plans, they had to be consolidated into a Direct Consolidation Loan, which then qualified for ICR and only ICR. Under OBBB, that pathway remains available only through June 30, 2026. After that, consolidating a Parent PLUS loan into a Direct Consolidation Loan results in an “excepted consolidation loan” that is ineligible for RAP and for every other income-driven plan going forward. The only repayment option left is the Standard 10-year plan.

The deadline is not July 1 and it is not an application deadline. The Direct Consolidation Loan must be disbursed, meaning processed, funded, and active, before July 1, 2026. Standard processing runs 30 to 90 days. The Department of Education’s own guidance recommended applying by April 1, 2026 to safely hit disbursement by June 30. That window is already closed as you read this. Any client who hasn’t applied yet is now racing the servicer’s processing calendar.

Who is on the cliff

Pull your client list for anyone over 50 with student debt in their household financial summary, then narrow to those with federal loans in a parent’s name rather than the student’s. If your intake hasn’t captured loan-holder-name detail, you have a separate problem worth solving.

Specifically at risk:

- Parents who borrowed Parent PLUS and never consolidated. They are on the Standard plan already and may be tolerating higher-than-necessary payments because they don’t know ICR exists.

- Parents who consolidated years ago but not into a Direct Consolidation Loan that includes their Parent PLUS. Some older consolidations don’t qualify.

- Parents who were in the SAVE litigation forbearance before the Eighth Circuit vacated SAVE in March 2026 and now sit in administrative limbo as the Department of Education prepares to issue 90-day transition notices starting July 1. They face the cliff regardless of which plan the Department auto-enrolls them in.

- Parents whose youngest is still in school. Any new Parent PLUS disbursement after July 1, 2026 breaks the existing consolidation’s IDR eligibility. This cohort has to make a decision, fund the remaining college years through private loans or cash, or take new Parent PLUS and forfeit IDR access on the entire portfolio.

For a $65,000 Parent PLUS balance, the difference between ICR and Standard repayment is approximately $400–$600 per month over a decade. For a household near retirement, that’s the difference between a workable plan and one that forces a delayed retirement date.

The 30-to-90-day race

If a client hasn’t applied for consolidation yet, the sequence is:

First, confirm whether they have Parent PLUS and what the current repayment status is. The most reliable source is a fresh NSLDS pull, which the Federal Loan Simulator imports directly into Liability Planner.

Second, initiate the Direct Consolidation Loan application through studentaid.gov. The application itself takes less than an hour. Servicer processing is the variable, 30 days on the fast end, 90 days on the slow end, and both SAVE-transition volume and the broader July 1 implementation are pushing processing times up.

Third, track the disbursement date. Application alone does not satisfy the rule. The consolidation must be processed, funded, and active before July 1, 2026. If a client applies today and the servicer quotes 90 days, they land exactly at the deadline with no margin. The right move is to confirm weekly and escalate if the timeline slips.

Fourth, enroll in ICR immediately on disbursement. Once consolidated, the loan is an excepted consolidation loan and ICR is the only income-driven option. That status carries through June 30, 2028, at which point ICR sunsets and the borrower transitions to IBR or RAP. Most Parent PLUS consolidators will find IBR the better choice in 2028 because IBR retains a 150% Federal Poverty Level offset that RAP does not. But that’s a 2028 decision, not a 2026 one.

What happens if they miss it

Any Parent PLUS borrower without a disbursed Direct Consolidation Loan on July 1, 2026 is permanently locked out of income-driven repayment and Public Service Loan Forgiveness. Only the Standard Repayment Plan remains, 10 years of fixed payments on the unconsolidated Parent PLUS principal. There is no future legislative or administrative path to rejoin IDR that currently exists in statute. If a borrower takes out a new Parent PLUS after July 1, 2026 and consolidates at that point, it creates a new excepted consolidation loan that is similarly locked out of RAP.

Advisors should not build a strategy on “double consolidation,” the historical loophole where a Parent PLUS borrower consolidated once into a Direct Consolidation, then consolidated that loan into another Direct Consolidation to strip the excepted classification. The OBBB statute is silent on whether that loophole is closed; servicer practice as of April 2026 generally refuses second consolidations of excepted loans; formal DoE rulemaking is pending. Telling a client to plan around a loophole that regulators may close retroactively is not defensible.

Advisor action checklist

This week:

- Run a book-wide query for clients over 50 with federal student debt in the household.

- For any identified client, confirm whether loans are Parent PLUS and whether a Direct Consolidation Loan exists.

- For unconsolidated Parent PLUS clients, send a single-paragraph email framing the cliff and requesting a 15-minute call.

Before the deadline:

- Submit Direct Consolidation Loan applications for every affected client immediately.

- Confirm the servicer has received the application and provide the client a written tracking summary.

- Run side-by-side ICR vs. Standard vs. RAP projections in Liability Planner so the client sees the stakes.

- Confirm the disbursement date for every submitted application and escalate if the timeline slips past June 30.

After July 1:

- For clients with a child still in school, model the new-Parent-PLUS trade-off: take the new loan and lose all IDR access, or fund the remaining years from other sources. This is now a permanent decision with no reversibility.

The one thing to remember

The RAP transition gets most of the public attention because SAVE is bigger and more visible. The Parent PLUS cliff is narrower and more severe. A SAVE borrower transitioning under the Department’s 90-day notice has alternative plans to choose from. A Parent PLUS borrower who doesn’t consolidate by June 30 has no recovery path, ever.

Model your parent-borrower clients in the Federal Loan Simulator today and catch the ones still on the cliff.

Sources: One Big Beautiful Bill Act (P.L. 119-21); Department of Education Dear Colleague Letter, July 18, 2025; Federal Register NPRM “Reimagining and Improving Student Education” (91 FR 5627, Jan. 30, 2026); Eighth Circuit ruling vacating the SAVE Plan (March 10, 2026); Department of Education press release announcing SAVE next-steps (March 27, 2026); Congressional Research Service Report IF13075.

This is informational content for licensed advisors. Specific guidance for any individual borrower requires their loan data and circumstances.

Model the 2026 rules for a real client.

Run RAP, the new Standard, IBR, PAYE, ICR, and PSLF side by side, verified to the cent, and hand the client a report. Free 7-day trial.

Run a real repayment plan for any borrower in minutes

Every number sourced, every path compared. Model RAP, the new Standard, IBR, PAYE, ICR and PSLF side by side.